Even the greatest proponents of laissez faire economics would admit that the market is not an end, but rather a means. Larry Kudlow's creed is "Free market capitalism is the best path to prosperity." That's right, its a path! So why have so many business leaders and financial media pundits attempted to create a belief that the market is something that must be preserved and nurtured? Isn't the market merely the collection of opinions expressed by dollars? If the government or the people choose to encumber, regulate or manage those opinions expressed in dollars is that not just another manifestation of the "market?" Is not the choice to not encumber, regulate or manage those opinions expressed in dollars also a factor of the "market? Most importantly, does it even matter?

Welcome to the deepest depths of this blog to date. A philosophical puzzle that seeks no solution other than to paint shades of gray that shall make the reader come to their own conclusion based in logic rather than borrowed rhetoric or sloppy undeveloped thoughts, if one hasn't done so to date. In fact, if the reader is not prepared for this type of philosophical self-reflection, come back next week and I will be back to suggesting solutions to the chasms in our economy, politics and country.

The point: The goal of any socioeconomic system, culture, government or process in general is a greater standard of living for its people. In defining the concept of standard of living, one must not only count wealth, but the purpose that wealth serves. In other words, standard of living is a mark on a barometer which measures the ability of a population to live. It begins on the low end with "attain what one needs" and culminates with "attain whatever one desires." It is nonsensical, or rather simply incomplete, to state a standard of living is money or tangible goods because the logical question is money and tangible goods for what purpose? It's money to be free, or it's money to exert power over people, or money to live a life of leisure, or money to create security, or whatever. Its not the money, its the end that the money makes reality that is the intention or goal.

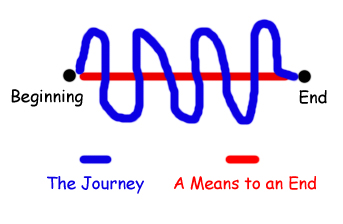

So, if money and tangible items are a vehicle, and the market is a vehicle to create or multiply that money, and the end is to maximize the standard of living of living of a population- the issue is thus centered around how we as citizens of a society get to that end in the most efficient and/or equitable manner. Remember, this particular article does not have the purpose of solving what is the best path to reach our end, it's merely to silence the annoying undeveloped statements of many who believe that the market is the end.

Two days ago I was reading an article from a brilliant financial planner who stated that the market shall prevail in destroying much of the Nation's wealth despite any efforts of the population to stave off such a doom through stimulus, the federal reserve and the treasury. The purpose of this article is not to argue whether or not the stimulus plan shall work, or whether Keynesian economic tools are effective, its merely to disprove the careless careless conclusion of this highly respected professional. If the market is not creating a greater standard of living, it is failing and not prevailing. Remember, the market having its way is nothing more than a runaway car as the intended destination is an aggregate maximized standard of living (not to be confused with an equal standard of living for all which is the goal of communism).

Now I know many readers would argue that in the long run the market is the best path to the end of standard of living, but I argue today that the long run is a summation of successes and failures. All I ask is that people admit that when the market is destroying wealth and creating a worse standard of living for those exposed to it, that it is in fact failing them at that time. After all, we should not treat the market as a deity. It is not always positive, it is not always correct. It has always worked itself out of its troubles, but it is neither a good or evil, it just is. In fact, the culmination of people's opinions as valued in money may not even be measurable as a provable existence. The idea of "the market" might simply be an expression of the common statement "it is what it is."

Whether it's the best we've got or the best we can ever get, the market and the management of its consequences should never be without criticism or reflection. The market deserves no sanctity or elevated stature. Its merely a mechanism. Sometimes it works to its intended purpose, sometimes not. It is a very strong mechanism; but, nonetheless one for the purpose of making our collective lives better. From here, the conclusion is yours to write.